How Much Down Payment Do You Actually Need to Buy a Home in Rochester, MI?

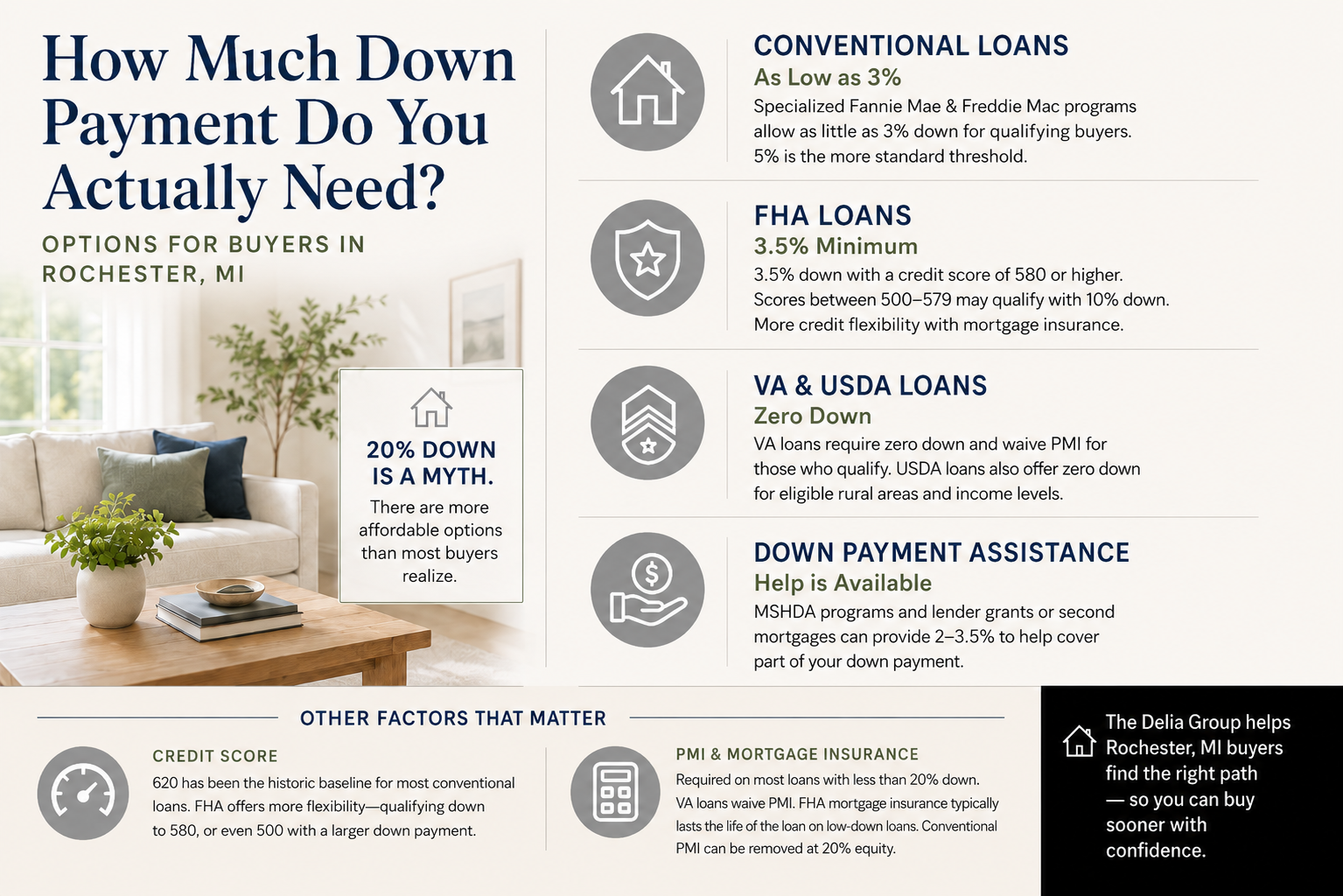

One of the most persistent myths in home buying is that you need 20% down to purchase a home. For most buyers in Rochester, MI, that simply isn't true -- and waiting to accumulate that level of savings often means delaying homeownership for years when you could have qualified sooner through a different path.

The Delia Group walks buyers through every available option so they can make a decision based on facts, not assumptions.

Conventional Loans -- As Low as 3%

Conventional loans through Fannie Mae and Freddie Mac have specialized products for qualifying buyers that allow down payments as low as 3%. These are typically tied to median income qualifications and come with specific eligibility requirements.

For most conventional borrowers, 5% is the more standard threshold. Above 20%, PMI goes away entirely -- but that's a long way from the baseline requirement.

FHA -- 3.5% Minimum, More Credit Flexibility

FHA loans require a minimum of 3.5% down for buyers with a credit score of 580 or above. Buyers with scores between 500 and 579 may still qualify with a 10% down payment. FHA is generally more flexible than conventional when it comes to credit score requirements -- but it does carry FHA mortgage insurance for the life of the loan on low-down transactions.

VA and USDA -- Zero Down

VA loans for qualifying veterans and active-duty service members require zero down payment -- and also waive private mortgage insurance entirely. This combination of no down payment and no PMI makes VA loans one of the most powerful homebuying tools available for those who qualify.

USDA loans (sometimes called rural loans) also allow zero down, but are tied to geographic eligibility -- the property must be in a qualifying rural or suburban area -- and income limits apply. For buyers who fit those parameters, USDA is an excellent option.

Down Payment Assistance -- MSHDA and Lender Programs

For buyers who have solid income and good credit but haven't been able to accumulate a full down payment, Michigan has resources specifically designed to help. MSHDA -- the Michigan State Housing Development Authority -- offers a down payment assistance program that can provide a meaningful chunk of the funds needed to purchase a home.

Additionally, individual lenders may offer their own grant programs or second mortgage products that cover 2 to 3.5% of the purchase price, often structured for FHA buyers. These programs have eligibility requirements and terms that vary by lender, but they're real and worth exploring.

Credit Score and PMI -- The Other Factors

A 620 credit score has historically been the baseline for most conventional programs. Fannie Mae has made changes to minimum score requirements, but the compensating factors that help buyers qualify are largely still tied to strong overall credit profiles. FHA is more flexible, with qualifying pathways down to 580 -- or even 500 with a larger down payment.

PMI -- private mortgage insurance -- is required on virtually all loans where the down payment is below 20%. The exception is VA loans, which waive PMI entirely. On FHA loans with less than 10% down, mortgage insurance premium is typically carried for the life of the loan. On conventional, PMI can be removed once equity reaches 20%.

The Delia Group Helps Rochester, MI Buyers Find the Right Path

There are more paths to homeownership than most buyers realize. The Delia Group works with buyers in Rochester, MI to identify which down payment option fits their financial situation -- and helps make sure they're not waiting longer than they need to.

📲 Ready to find out what down payment options are available for your situation? Reach out to The Delia Group today.