FHA vs Conventional Loan -- How Rochester, MI Buyers Should Think About This Decision

One of the most common questions buyers ask before they start seriously shopping for a home in Rochester, MI is a deceptively simple one: should I go FHA or conventional? The answer -- as The Delia Group is quick to point out -- is that there isn't a universal right answer. It depends on a combination of factors that are specific to you and to the home you're trying to buy.

Here's the framework for thinking through the decision.

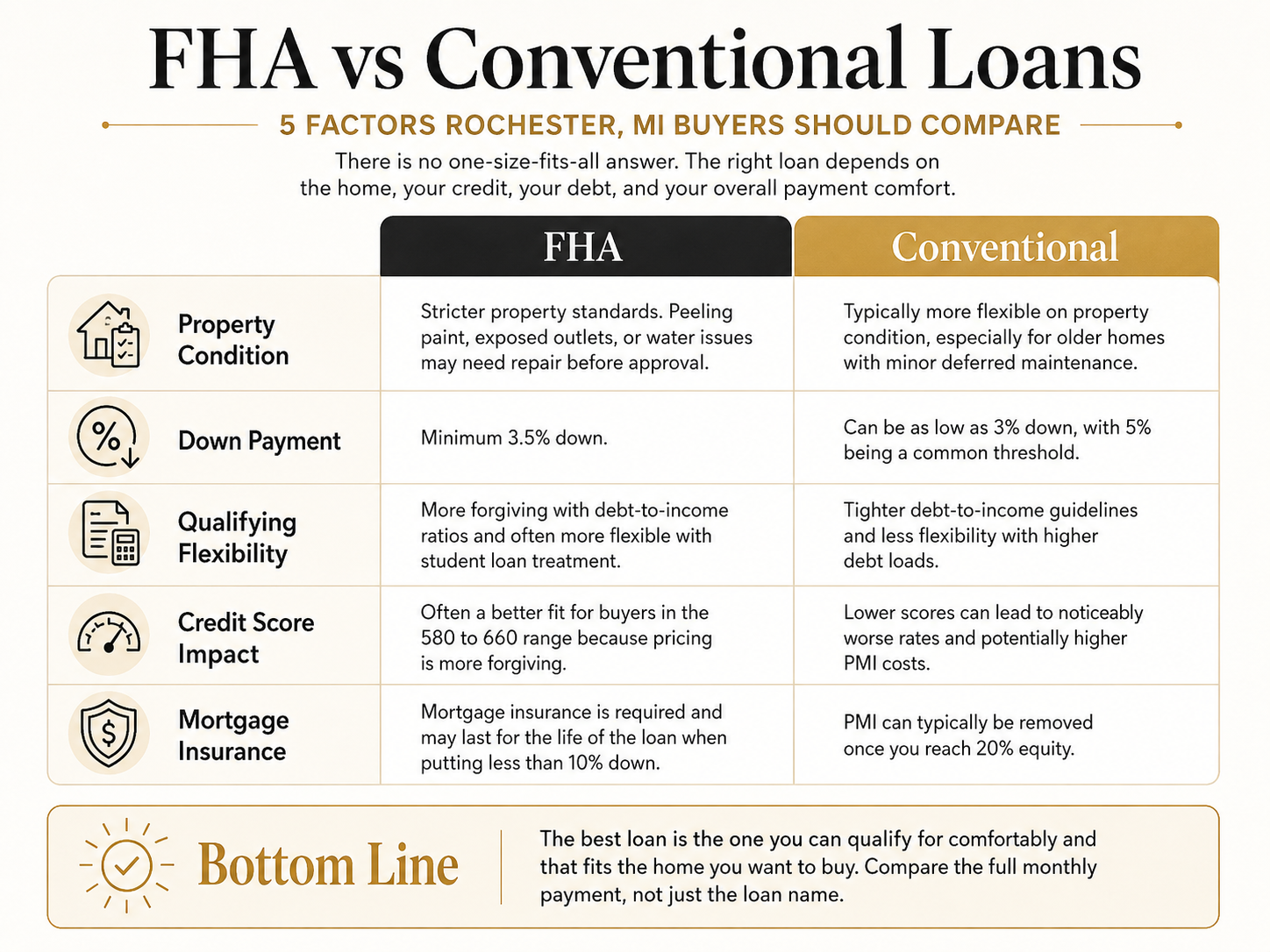

Factor 1 -- Property Condition

The condition of the home you're purchasing is actually one of the first things to assess when deciding between FHA and conventional -- and it's a factor a lot of buyers don't consider upfront.

FHA loans come with property condition requirements that conventional loans typically don't carry. On older homes, issues like peeling paint, uncovered electrical outlets, or water intrusion near the foundation can hold up or even block FHA approval until they're repaired. Some issues are minor and relatively easy to address before closing. Others -- like water-related problems -- can be more costly and time-consuming.

If you're buying an older home that might have some deferred maintenance, it's worth understanding whether an FHA appraisal could flag issues before you're committed to that financing path.

Factor 2 -- Down Payment

Down payment requirements are often cited as the key difference between FHA and conventional -- but in practice, they're closer than most people assume. FHA requires a minimum of 3.5% down. Conventional loans through Fannie Mae and Freddie Mac have specialized products that allow as little as 3%, with 5% being a standard conventional threshold.

The down payment difference between the two is relatively small. The bigger differentiators tend to be in qualifying flexibility and how mortgage insurance is structured.

Factor 3 -- Qualifying Flexibility and Debt-to-Income

FHA is significantly more flexible than conventional when it comes to debt-to-income ratios -- the calculation that measures your total monthly debt obligations against your gross monthly income. FHA will allow higher ratios and often treats certain debts, including student loans, more generously than conventional underwriting guidelines.

Conventional loans have harder stops on debt-to-income ratios. If your overall debt load is high relative to your income, FHA may be the path that gets you to qualification -- even if it doesn't feel like the "premium" option.

Factor 4 -- Credit Score Impact

Credit score affects both loan types -- but the way it affects pricing is very different. With conventional loans, the pricing tiers are steep: a lower credit score means meaningfully worse interest rates and potentially higher PMI costs. The penalty for a lower score on a conventional loan is significant.

FHA pricing is more graduated and generally more forgiving of lower credit scores. For buyers whose scores are in the 580 to 660 range, FHA often produces a better overall payment even after accounting for FHA's mortgage insurance structure.

Factor 5 -- PMI and Mortgage Insurance

Both loan types require some form of mortgage insurance when the down payment is below 20% -- but how that insurance works differs considerably. Conventional PMI can drop off once you reach 20% equity in the home. FHA mortgage insurance on loans with less than 10% down is typically carried for the life of the loan.

The monthly cost of mortgage insurance also varies based on your down payment amount, your credit score, and which product you're using. The total payment picture -- principal, interest, taxes, insurance, and mortgage insurance -- is what The Delia Group helps buyers evaluate before they make a final decision.

The Real Question -- Which One Can You Qualify For Comfortably?

The Delia Group frames the FHA vs conventional decision this way: there isn't a better or worse option. There's only which one works for your specific circumstances. The goal is to qualify you for a loan that not only gets you into the home but produces a payment that's genuinely comfortable for your financial situation.

If you're trying to work through this decision for a Rochester, MI home purchase, The Delia Group is ready to help you navigate it.